Jarrett Parr is a Financial Systems Implementer for SuiteDynamics, a NetSuite solutions provider. He enjoys analyzing and improving processes for both our company and clients. He also loves solving accounting and financial problems for growing businesses. Jarrett lives in Madison, WI, with his wife, Abbie, and their golden retriever, Clark.

A Quick Guide to Costing Method Types and NetSuite Accounting Software

NetSuite accommodates several different costing methods, so a customer can choose what works best for their business. But each one has its pros and cons.

As every business leader knows, costing methods are crucial. The method a company chooses determines the price of its goods, the taxes it will pay, the profits it will make, the forecast for its future revenue, and more.

That’s why companies must think through their costing process—particularly if using an enterprise resource planning (ERP) system like NetSuite. Various ERPs handle costing methods differently, so you have to choose a process that’s not only right for your business but also right for your software.

At SuiteDynamics, we know that’s a complicated choice—but we can help. Our company works with NetSuite to implement and customize NetSuite software. If your company uses a NetSuite ERP, we can help you decide which costing method will work best for your operations. Below, we’ve listed five of the main methods used in the system, their pros and cons, and how to select one in the system.

Read through the guide, and then schedule a free consultation with our team. We employ financial experts who can help organize and streamline your financial processes within NetSuite, so your company can become better, stronger, and more successful.

Key Takeaways

- Costing methods impact all areas of business finance. Your chosen costing method influences product pricing, profits, taxes, and overall revenue forecasts, making it a critical decision.

- Choosing a method that fits your ERP is essential. Different ERPs like NetSuite handle costing methods uniquely, so it’s crucial to align yours with what your software best supports.

- SuiteDynamics can guide you through NetSuite’s costing options. If you're using NetSuite, SuiteDynamics offers consultation to help you choose and implement the right costing method tailored to your business.

- NetSuite has five main costing methods. FIFO, LIFO, Average, Standard, and Serialized costing. Each has unique pros and cons and can be selected per inventory item.

- Costing methods have pros and cons. For example, FIFO suits perishable goods but may raise taxes during inflation; LIFO can cut taxes but isn’t globally accepted; average costing is simple but can be less accurate; standard costing helps with planning but needs perfect data; and serialized costing is super precise but works only for unique items.

- Expert guidance can simplify the process. SuiteDynamics provides free consultations with financial experts to help optimize and streamline your NetSuite costing, making inventory management more efficient and accurate.

What Is a Costing Method?

An inventory costing method is basically the way a company decides what its products “cost” over time. Since various expenses (like materials) can increase and decrease quite a bit, these methods help figure out what each product a company sells actually costs. That number is significant because it affects how much profit the business says it makes and what it pays in taxes.

Lisa Schwarz, NetSuite’s Senior Director of Global Product Marketing, explains in an article that the costing process helps make critical inventory management decisions.

“Inventory costing is a part of inventory control technique,” she writes. “Proper inventory control within a supply chain helps reduce the total inventory costs and assists in determining how much product a company should carry. All this information helps companies decide the needed margins to assign to each product or product type.”

Accountants also use generally accepted accounting principles (GAAP) to ensure companies don’t overstate these inventory costs.

Costing Method Varieties Used in NetSuite

Many industries have preferred costing methods, but that doesn’t mean you have to stick with the one used by yours. In fact, NetSuite accounting software lets you choose a costing method per item, so you don’t even have to apply the same one to all inventory. Let’s explore your options.

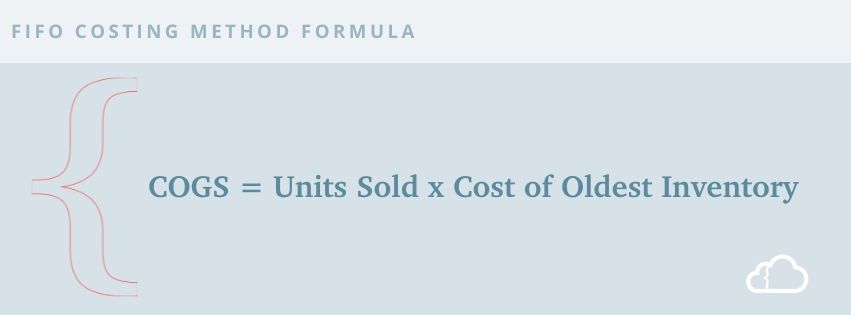

FIFO

Companies traditionally use the “First In, First Out” costing method for perishable goods. A business using this method will maintain a ledger for every item purchased. (NetSuite does this automatically.) That ledger tracks and calculates the cost of goods sold (COGS) using the price of items purchased from oldest to newest.

Example: On day one, you purchase 10 widgets for $5. On day two, you buy 10 more for $6. On day three, you sell 15. The COGS for the first 10 widgets will be $5, and the COGS of the remaining five widgets will be $6.

Pros

- Saves time and money because costs are calculated using the cash flows of first-used items instead of exact costs.

- Widely used and accepted.

- Easy to understand.

- Practical approach since it helps determine the COGS at the point of sale.

- Makes manipulating income difficult when it’s reported on financial statements.

- Shows increased gross and net profits when costs rise.

Cons

- Can result in higher tax liabilities if the profits grow during inflation.

- May not work well during hyperinflation.

- Requires significant amounts of data, raising the risk of clerical errors.

- May not work for goods with fluctuating price patterns.

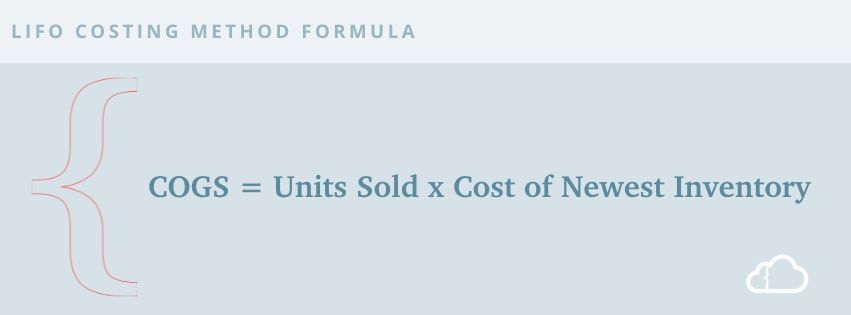

LIFO

The opposite of FIFO, the “Last In, First Out” costing method calculates the COGS, starting with the cost of the most recently purchased item and working backward. Note that the International Financial Reporting Standards (IFRS) don’t endorse this method. You can only use it under the United States’ Generally Accepted Accounting Principles (GAAP).

Many companies choose LIFO because costs increase in a typical inflationary environment, leading to a higher cost of goods and lower profit per item sold. This, in turn, lowers the tax burden as net income reduces.

Example: On day one, you purchase 10 widgets for $5. On day two, you buy 10 more for $6. On day three, you sell 15 widgets. The COGS for the first 10 widgets will be $6, and the COGS of the remaining five will be $5.

Pros

- Compares recent costs to current revenues, improving the quality and reliability of earnings.

- Decreases the likelihood that a price decline will affect net income.

- Alleviates profit overstatement and, thus, lowers the amount of income tax owed.

Cons

- Drops reported earnings during inflation.

- Allows for easy earnings manipulation.

- Allows the working capital position to look worse than it is because this method understates inventory.

- Can encourage poor buying habits since companies must buy goods in large quantities to avoid reported income inflation and higher tax payments.

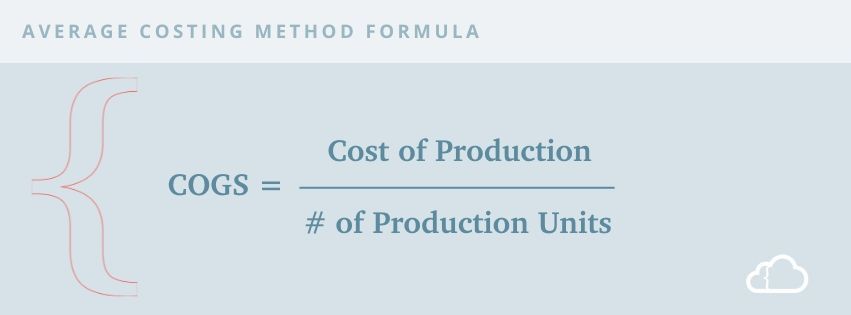

Average Costing

Average costing, also known as weighted average costing, calculates the COGS by totaling the cost of all inventoried items and dividing it by the total quantity. This costing method helps mitigate the effects of price fluctuation by incorporating the costs of older inventory into that of newer merchandise.

Example: On day one, you purchase 10 widgets for $5. On day two, you buy 10 more for $6. Your average widget cost is now $5.50. On day three, you sell 15 widgets for $10 each. Your COGS for each item would be $5.50.

Pros

- Simplifies calculation and record-keeping.

- Easily processes high volumes of inventory orders.

- Requires little to maintain inventory costs or calculate COGS for sales.

- Doesn’t require ongoing maintenance costs.

- Allows users to run ad-hoc or scheduled searches to find data or produce inventory cost reports.

- Widely accepted and permitted by several accounting standards.

- Useful when you can’t tell one batch of goods from another since all costs are averaged.

- Can produce data that NetSuite accounting software automatically converts into various currencies.

Cons

- May produce ending inventory cost that significantly differs from prevailing prices at a certain date, thus hampering decision-making.

- May use a rounding process for long decimals that can distort gross profit and current asset figures for large transaction volumes.

- Can cause frequent price changes if you’re using a cost-plus-pricing strategy.

- Makes it challenging to determine an item’s value since all goods lose their identity during averaging. This can cause problems when a unit’s age factors into the pricing.

- Can still be affected by cost fluctuations if you buy large quantities at the start or end of a period, particularly if the cost of those purchased goods varies significantly from the rest of the period.

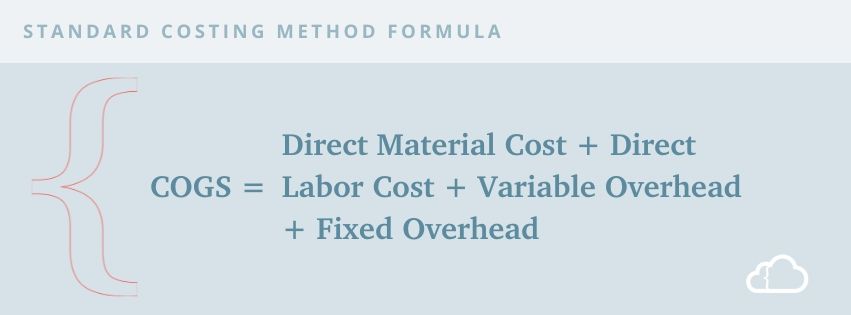

Standard Costing

Standard is the traditional costing method for manufacturers. It bases the COGS on a predetermined, estimated cost for each inventory item. Then, when actual costs differ from the estimate, the difference is captured in a variance account. Eventually, the company must reconcile that account to get an accurate idea of its current inventory value.

Example: A widget is composed of two components, part A and part B. At the beginning of the year, you estimate part A will cost $2 and part B will cost $3, so the estimated cost of a widget is $5. Therefore, the COGS for the product will be $5.

However, after three months, data shows the actual cost of part A is $4. A variance account will capture the difference in actual cost versus expected cost. Consequently, your COGS would remain $5, and you would also have a variance account for part A, debited $2. After an inventory reconciliation, you would account for the debit in the variance account and add it to the inventory cost of part A, making it $4 and the price of the widget $7.

Pros

- Can be compared with actual cost to measure efficiency.

- Can measure employee productivity and efficiency, depending on positive or negative variances.

- Fixes standards for specific activities, encouraging employee efficiency.

- Helps estimate production costs when the actual production cost isn’t known.

- Allows management to control production and decide cost elements, like wages and material purchases.

- Emphasizes cost-effectiveness and quality, improving production.

- Identifies waste in the production process.

- Helps accurately estimate the cost of new products.

Cons

- Uses standards that are difficult to determine, and incorrect standards can cause losses.

- Uses standards that must be revised periodically to reflect current marketing conditions, technology, and consumer habits.

- Requires specialists and experts to set standards.

- Expensive to use since standards must be carefully researched and analyzed.

- Only viable when you use budgetary techniques.

- Only suits companies with uniform production and set quality.

- Requires three steps for every inventory item entered with NetSuite accounting software.

- Can become frustrating since NetSuite accounting software doesn’t allow any actions until you set a predetermined standard on an item bracket. This includes transaction processing and receiving an item against a purchase order.

- Tedious for users with inventory in tens or hundreds of thousands.

- Requires that you perform a standard cost rollup with NetSuite accounting software to update the assembly cost (process shown later in the post).

- Requires that you revaluate standard cost inventory in NetSuite to calculate an updated inventory cost (process shown later in the post).

- Can take hours or days to complete in NetSuite if you have an extensive inventory. This can cause a lag in data accuracy.

- Can only be done using a single currency at a time, creating difficulties for multinational corporations.

Note: Standard costing requires nearly perfect data to work correctly. However, companies without flawless data can use a custom field in NetSuite that mimics standard cost functionality.

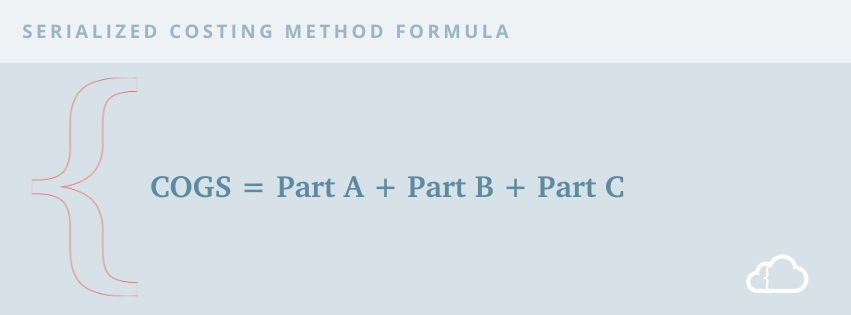

Serialized Costing

With this costing method, an ERP accounting system can track each part or item individually using unique serial numbers. If the parts are used in a project, the COGS for the project will reflect the exact sum of every individual part used.

Example: Widget 001 was built with parts A ($3), B ($4), and C ($5) for a total COGS of $12.

Pros

- Highly accurate since you can record exact costs in inventory records.

- Offers greater accuracy with gross profitability since an item’s actual cost is used for the COGS when the serialized item is sold.

Cons

- Tedious for any business with a large inventory.

- Can only be used with lot/serialized item types.

- Can’t be used to track all items in a company’s system because not all have unique lot/serial numbers.

- Restricted to specialized items and businesses involved in equipment, cars, etc.

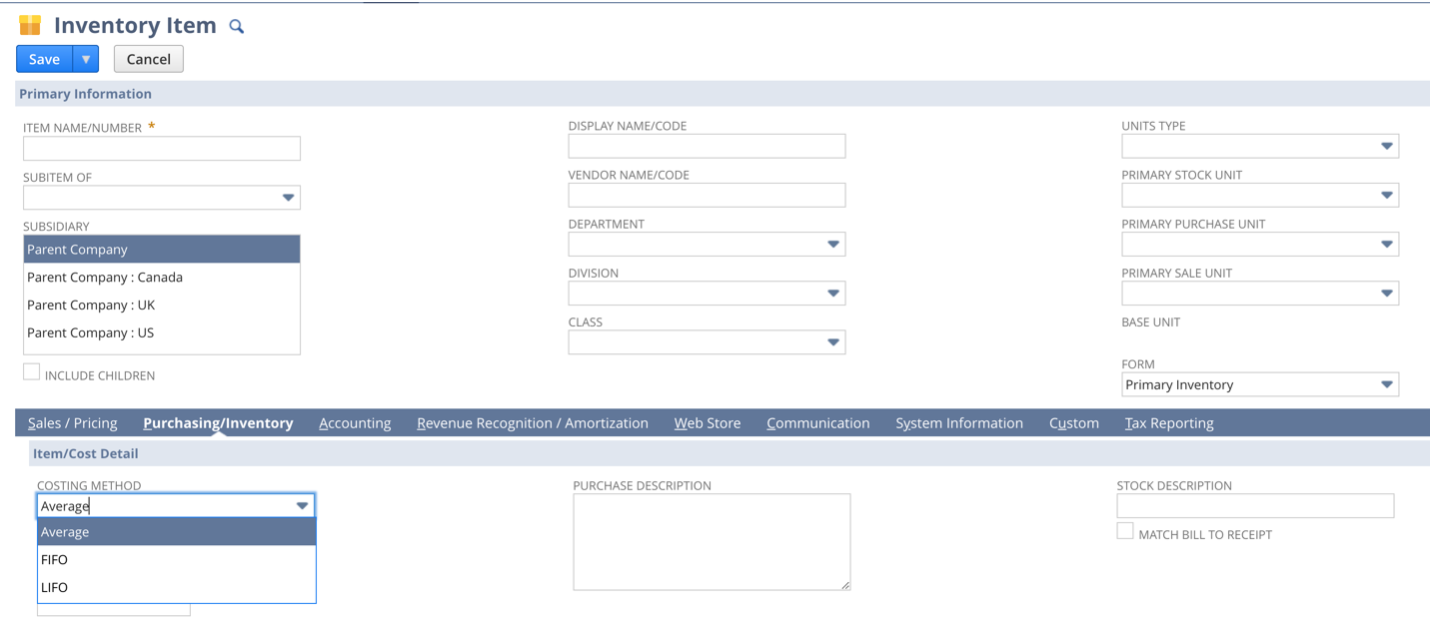

Selecting Costing Methods with NetSuite Accounting Software

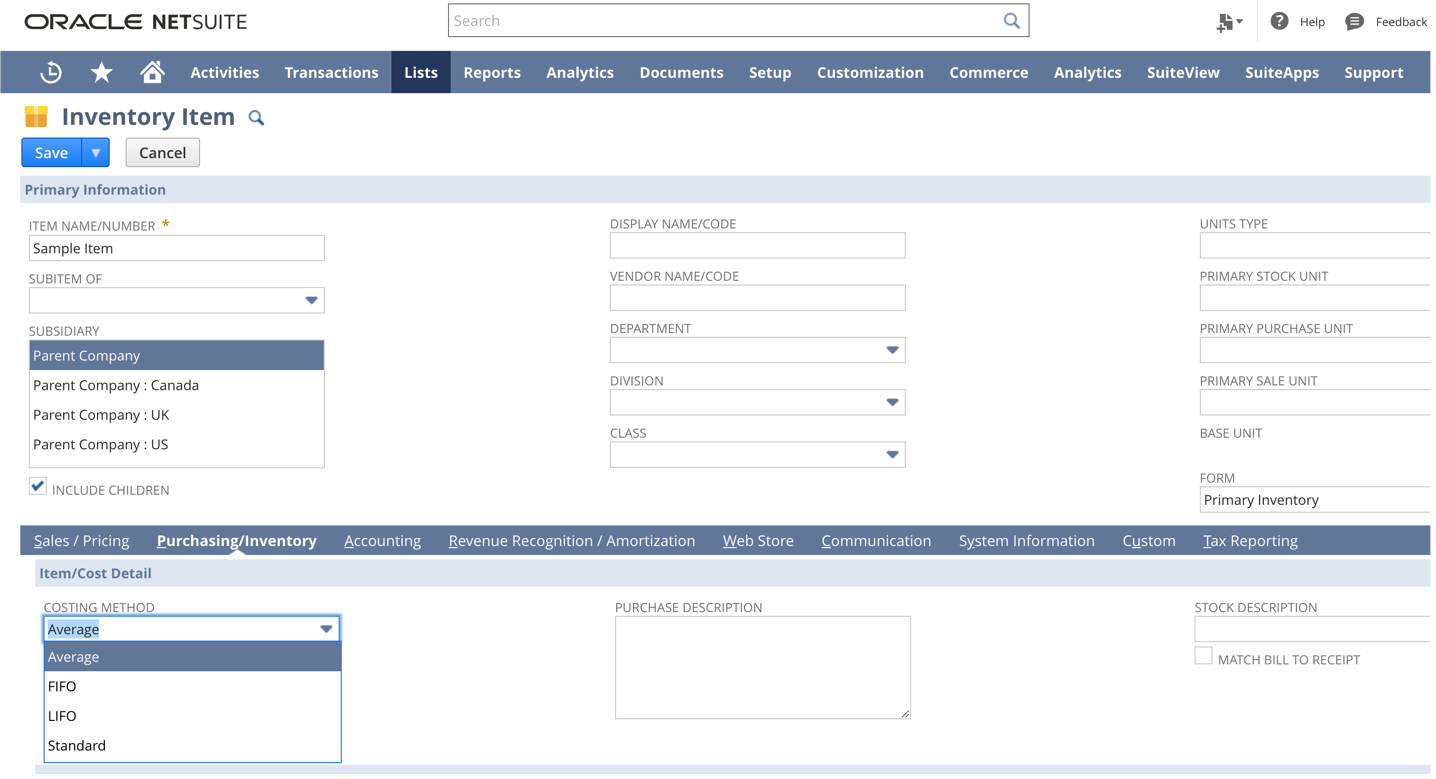

Select a costing method when creating an item. You can find the Costing Method dropdown menu under the Purchasing/Inventory subtab.

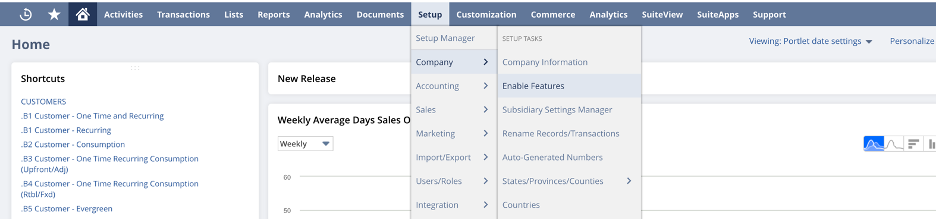

By default, standard costing won’t be enabled in NetSuite. To enable it, navigate to Setup > Company > Enable Features.

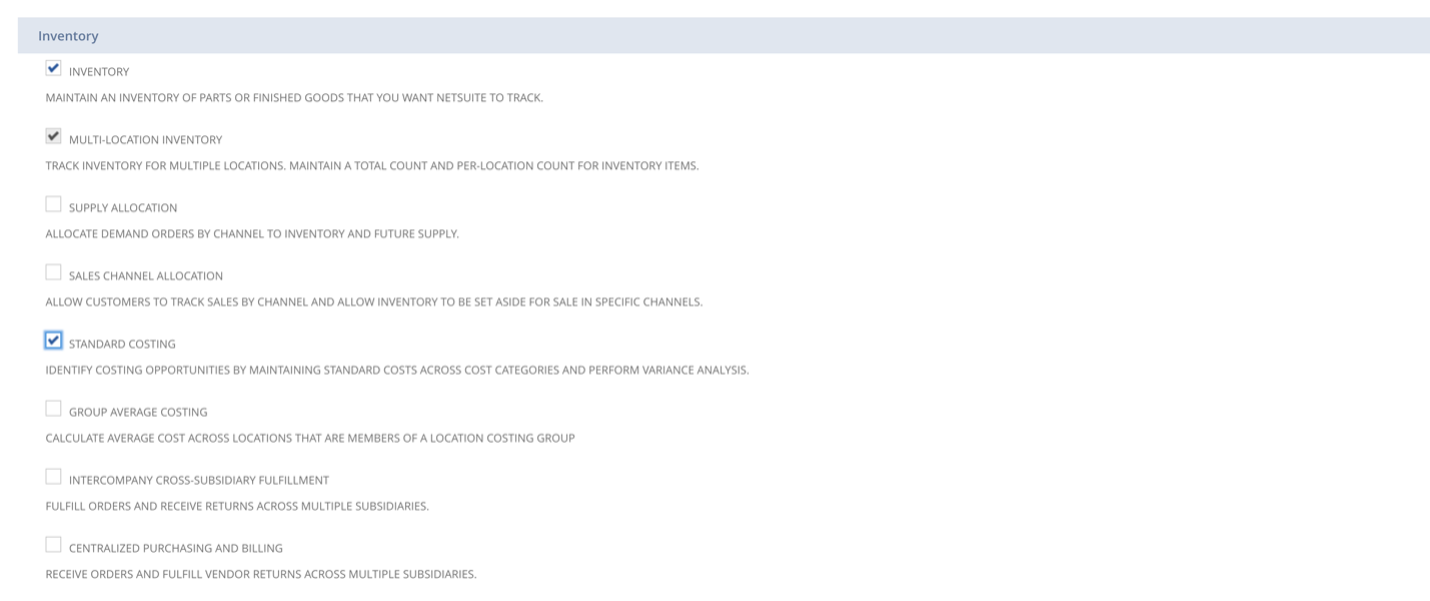

Then, click on the Items & Inventory subtab.

Scroll down to the Inventory section and check Standard Costing. Then, click Save.

Now, standard costing will be available from the Costing Method dropdown.

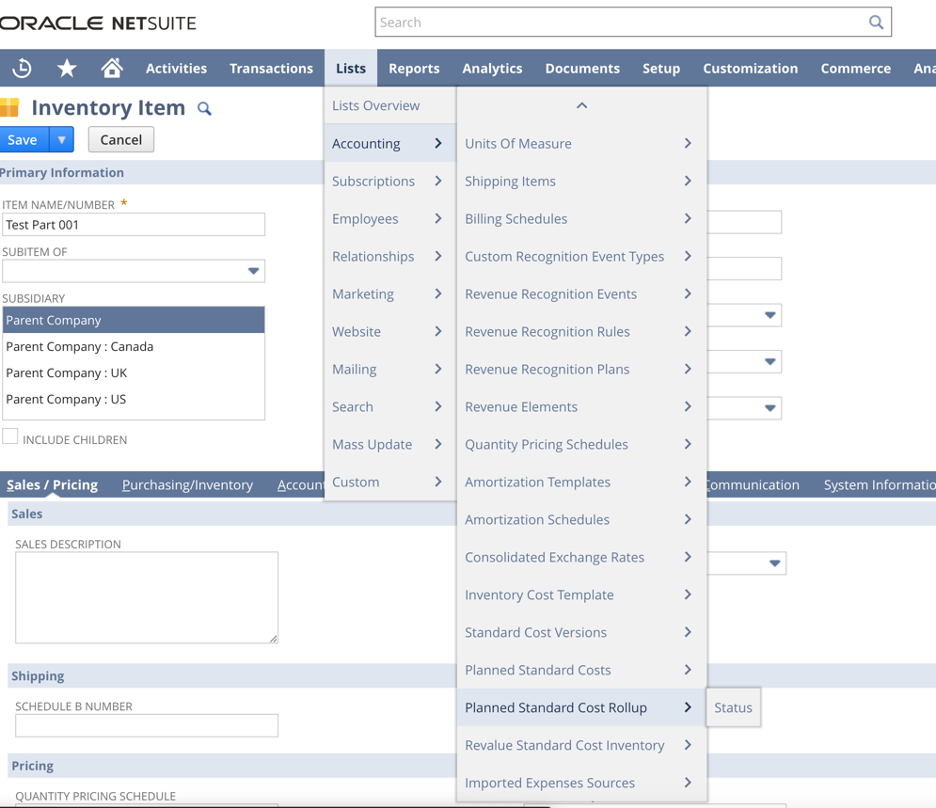

Performing a Standard Cost Rollup in NetSuite

Navigate to Lists > Accounting > Planned Standard Cost Rollup.

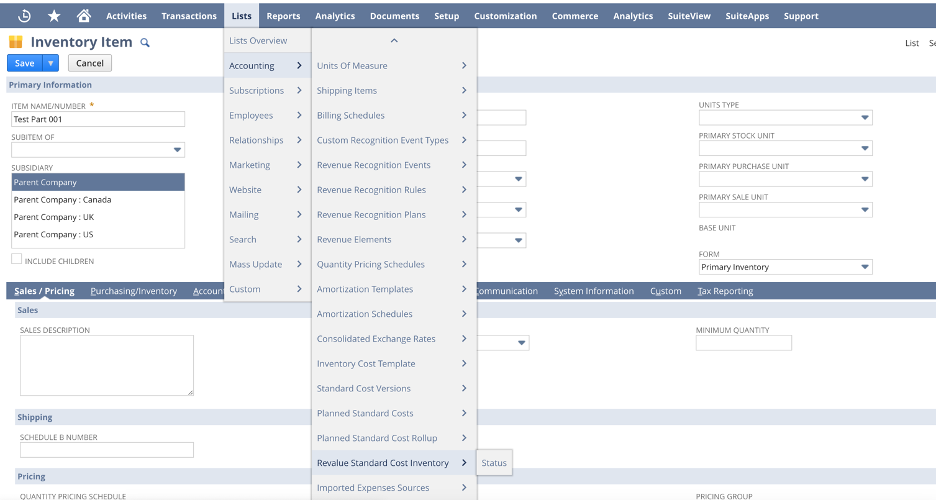

Performing a Revaluation of Standard Cost Inventory in NetSuite

Navigate to Lists > Accounting > Revalue Standard Cost Inventory.

The right costing method may determine whether your business experiences profits or losses, so choose carefully. The SuiteDynamics experts can help determine which will best serve your company in the market and in NetSuite. Schedule a free consultation with our team, and let us know how we can help.

Frequently Asked Questions

1. Which costing method is best for tax reduction purposes?

LIFO typically results in lower taxable income during inflationary periods because it assigns higher, more recent costs to goods sold. However, it's only permitted under US GAAP, not International Financial Reporting Standards (IFRS). Average costing can provide a middle ground with moderate tax implications, as it smooths out price fluctuations by averaging all inventory costs. Standard costing, while not typically chosen primarily for tax purposes, can help manufacturers identify and address cost variances that might ultimately reduce taxable income through improved efficiency.

2. Can a company change its costing method after implementation?

Yes, but it would involve an enormous amount of work. A costing method cannot be changed on an item once set, requiring you to recreate entirely new items from scratch. The switch to begin using these new items would be similar to a go-live, likely requiring a go-dark period for business operations while you load new items and deactivate old ones. This can also impact any reports or metrics that utilize items and can require additional steps for accurate historical reporting. It would be a significant undertaking, so it’s better to get your costing method right before going live.

3. How do costing methods impact financial reporting and business decision-making?

Costing methods directly affect key financial metrics, including gross profit, net income, inventory valuation, and tax obligations. FIFO typically shows higher profits (and potentially higher taxes) during inflationary periods, while LIFO shows lower profits. Average costing tends to stabilize these metrics by blending costs over time, which can provide more consistent reporting periods. Standard costing offers manufacturers unique insights through variance analysis, revealing efficiency problems and opportunities for process improvement. These differences influence critical business decisions about pricing strategies, purchasing patterns, and expansion plans. Companies should select a method that complies with relevant accounting standards and provides the most useful information for their specific industry, inventory characteristics, and management objectives.

Blow Away the Competition

Stop fighting a software system that's working against you. Instead, enjoy the benefits of an ERP that knits your operations together seamlessly and provides the data and analysis you need to trounce your competition.

We know you can rise in your industry.

Team up with SuiteDynamics to develop the ERP system your business needs. As NetSuite solution providers, we license, customize, and implement NetSuite ERP software for clients in any industry.

The partnership doesn't stop there. We can continue working together long after go-live, maintaining the system, training staff, and adjusting the software to accommodate your expansion. Start by scheduling a free consultation with our team.

We pull information from NetSuite material, SuiteDynamics experts, and other reliable sources to compose our blog posts and educational pieces. We ensure they are as accurate as possible at the time of writing. However, software evolves quickly, and although we work to maintain these posts, some details may fall out of date. Contact SuiteDynamics experts for the latest information on NetSuite ERP systems.

Failed NetSuite implementations are almost never about the software. NetSuite runs tens of thousands of businesses. The platform works. So when an implementation goes sideways because of blown budgets, missed go-live dates, or system nobody trusts yet, the instinct to blame the tool is understandable. But it's usually wrong. The failure typically lives in how the system was implemented, and in our experience rescuing troubled projects, it almost always traces back to one of five root causes. 1. The scope was underestimated from day one A lot of failed implementations were doomed before kickoff. The project was sold as a simple, clean migration, with standard configuration. Maybe a few months of work. Then reality hits when the legacy data was messier than anyone admitted. The "standard" processes turned out to have a dozen exceptions each, and custom requirements surfaced mid-project. When scope balloons after the contract is signed, two things happen: the budget and timeline blow up, and the team starts cutting corners to hit dates that were never realistic. Neither ends well. 2. The system was configured without business context This one is subtle, because on paper everything looks fine. The consultants knew NetSuite inside and out, and the configuration follows best practices, yet the system fights your team at every turn. The problem is that knowing NetSuite isn't the same as knowing your business. If the people configuring the system never sat with your warehouse team, never traced an order from quote to cash, or never asked why you do things the way you do, you end up with a technically correct system built for a company that isn't yours. 3. Data migration was rushed or sloppy Garbage in, garbage out. It's a cliché because it keeps happening. The trap is that a data migration can be technically "complete," with every record moved and every checkbox ticked, while you still have unusable data. Duplicate customers, items with wrong costing, or open transactions that don't reconcile are all things we see regularly during implementation rescues. We even see historical records mapped to the wrong accounts. The migration passed, but your team can't trust the subsequent reports. Bad data quietly poisons everything downstream, and it's often the last problem anyone diagnoses because the migration was marked "done" months ago. 4. Nobody actually tested against real workflows There's a big difference between "the feature works" and "the feature works for how we operate." Failed implementations are full of the first and starved of the second. Real testing means running your actual scenarios. If features were validated in a vacuum (or worse, marked complete without validation at all) the problems don't show up until go-live, when they're most expensive to fix. 5. No one owned the project end-to-end Implementations are long, and it's not uncommon for consulting firm swaps team members during a project. Each handoff loses context, and eventually nobody on either side holds the full picture of what was decided, why, and what's still open. Missing ownership is why so many troubled projects feel unaccountable. Every issue is somebody else's decision from six months ago, and no one can explain the reasoning behind it. The fix depends on the point of failure If your NetSuite implementation is in trouble, the temptation is to start fixing symptoms by patching reports, adding workarounds, and retraining users. A real rescue starts with diagnosis to figure out which of these five failures happened on your project. Treating the wrong root cause just adds cost on top of a project that's already over budget. The good news: implementations can be rescued . The system underneath is solid. What went wrong is fixable once you know exactly what went wrong. Schedule a rescue assessment with our team to get started on the right path.

Job shop manufacturing is a production strategy focused on customization over volume.

The future of manufacturing planning is in systems designed to flex and reflect how work actually happens in job shops with tools like Dynamic Job Shop.

Explore Esusu's partnership with SuiteDynamics to enhance financial processes. Schedule a consultation to see how your business can thrive with NetSuite solutions.

Spreadsheets built modern business. For decades they served as the unofficial operating system of job shops and custom manufacturers everywhere. They are flexible, familiar, and just comfortable enough to feel like a real solution. In the early days of a growing shop, they genuinely work. But as make-to-order complexity increases, as custom BOMs multiply, lead times tighten, and engineering revisions pile up, spreadsheets strain under the pressure. Every job is different, but spreadsheets want everything to be the same. In make-to-order environments, no two jobs are identical. Unique BOMs, custom routings, variable material costs, different setup requirements, customer-specific specs. Spreadsheets, though, thrive on repetition and standardized rows. So the more variation you introduce, the more tabs you create. The more exceptions you add, the more manual overrides appear. The more formulas you patch together, the more fragile the whole thing becomes. Eventually, the file turns into something only one person truly understands. That’s a liability, not a system. Capacity becomes a guessing game. In make-to-order shops, capacity isn’t theoretical. It’s constrained by reality. Machines go down. Operators vary in skill. Setup time fluctuates from job to job. Rush orders blow up carefully planned weeks. Spreadsheets struggle here because they’re built on static inputs. You can build a beautiful planning sheet with machine-hour allocations, but unless it dynamically adjusts for real-time job status, operator availability, overlapping resource conflicts, and maintenance downtime, you’re not really planning. You’re forecasting best-case scenarios. And that’s exactly how shops overpromise delivery dates and end up paying for it later in overtime and expediting costs. Engineering changes don’t cascade cleanly. Change is a constant in make-to-order manufacturing. A customer tweaks a dimension, a material substitution becomes necessary, or a tolerance tightens halfway through production. In an integrated system, that change automatically updates BOMs, routings, cost projections, and scheduling impact all at once. In a spreadsheet environment, it depends entirely on who remembers to update which tab. A routing might change without adjusting the labor estimate. A material substitution might never feed into the margin calculation. A lead-time adjustment might not reach the production schedule until it’s too late. These small disconnects multiply quickly, and because spreadsheets have no enforced relationships between data sets, the errors don’t announce themselves. Institutional knowledge becomes a single point of failure. Ask most growing job shops who owns the master spreadsheet and you’ll get a name. One estimator, planner, or operations manager who has become the living interpreter of years’ worth of embedded formulas, assumptions, and logic that nobody else fully understands. This works fine until it doesn’t. When that person goes on vacation, gets sick, or leaves, the shop loses operational clarity. In an environment already defined by complexity, having critical knowledge live inside one person’s mental model of a file is an inefficient bottleneck. Visibility stops at the file boundary. Spreadsheets are static snapshots. Make-to-order manufacturing is anything but. Without real-time feedback loops, shops find themselves unable to answer questions that should be simple: Are we actually on track this week? Which jobs are consuming more labor than quoted? Where is the bottleneck right now? Which customers consistently drive margin compression? When performance data doesn’t flow automatically from the floor back into quoting and planning, improvement stalls. You can’t refine what you can’t see. Here’s the thing about spreadsheet failure in manufacturing… it’s not dramatic. It’s gradual. First the files get slow, then fragile, then opaque. By the time leadership feels the real pain through late shipments, squeezed margins, and rising overtime, the architectural issues are widespread. Make-to-order manufacturing demands systems that understand relationships: how a routing affects capacity, how a BOM revision affects cost, how a delayed job cascades through the rest of the schedule. The question most shops ask is whether they can make the spreadsheets work. The better question is what it’s actually costing to keep them. The most resilient make-to-order manufacturers are building systems that preserve flexibility without sacrificing the visibility needed to actually run the business. Adaptability is the advantage.

In custom manufacturing , when systems break down, profit rarely disappears all at once. It leaks. Quietly, repeatedly, and often in ways that never show up clearly on any report. Walk into almost any fabrication shop and you’ll hear some version of the same story: the backlog is strong, revenue looks good, we’re staying busy. And yet the margin feels thinner than it should. For job shops running custom work, profitability doesn’t usually collapse because of one bad decision. It erodes through small, daily inefficiencies buried inside quoting, scheduling, engineering changes, and the gap between what was planned and what actually happened on the floor. Here’s where shops most commonly lose efficiency, and how to get it back. The quote that was almost right. For custom orders, every quote is a prediction, and predictions are dangerous when they’re disconnected from real shop-floor data. Outdated labor standards, underestimated setup time, material prices that changed since the template was built, and capacity assumptions based on average weeks instead of current reality. These errors are each small on their own, but a 4% underestimate on labor here, a missed secondary operation there, add up across hundreds of jobs. Small errors compound into real margin loss. The best-performing shops treat quoting as a living system fed by actual job performance data, not static spreadsheets that nobody updates. Capacity that looks available but isn’t. On paper, there’s open space on the schedule. In practice, that open week includes a machine down for maintenance, a senior operator on vacation, two complex jobs already competing for the same bottleneck, and a rush order someone verbally committed to last Thursday. Without finite capacity planning, shops routinely overcommit based on theoretical machine hours rather than real-world constraints. The fallout is predictable: overtime spikes, expedited shipping costs, re-sequencing chaos, and exhausted operators. Margin shrinks not because the shop is incapable, but because it’s planning in averages. Engineering changes that never get repriced. Designs evolve. A hole moves, a weld spec changes, or a tolerance tightens. Each adjustment has a cost. But many shops hesitate to reprice midstream, worried about damaging the customer relationship, and end up absorbing the extra labor and rework time instead. Do this enough times and it becomes a cultural norm: “we’ll just take care of it.” That’s margin erosion disguised as good service. High-performing job shops track engineering change impact in real time and make repricing decisions based on data rather than discomfort. Setup time hiding in plain sight. In low-volume, high-mix environments, setup time is often the silent killer. When shops don’t track setup separately from run time, assume it’ll all come out in the wash, and never refine their routings based on what actually happened, they end up underpricing complexity. In job shops producing one to fifty unit runs, setup can represent a disproportionate share of total labor. If it isn’t measured accurately, it can’t be priced accurately. The spreadsheet layer nobody talks about. Most shops run a hybrid environment where the ERP handles transactions and spreadsheets handle reality. Capacity lives in one file, quoting assumptions in another, and actual job performance in someone’s head. This creates invisible disconnects. Quotes not aligned with current routing, schedules that don’t reflect real constraints, and historical performance that never feeds forward into better decisions. Each disconnect feels manageable in isolation. Collectively, they create margin leakage that leadership can feel but can’t quite locate. What makes all of this so frustrating isn’t that shop owners don’t care. It’s that they can’t see clearly enough to act decisively. Without integrated visibility across quoting, routing, capacity, and quality, operators run on instinct. And instinct works remarkably well until scale and complexity outpace it. The shops that consistently outperform aren’t necessarily the biggest or the busiest. They operate with clarity and consistency. Fewer assumptions and more decisions based on reality. In a manufacturing landscape where lead times keep shrinking and customers expect speed and precision at the same time, margin won’t be protected by effort alone.

Every manufacturing leader has lived this moment: The schedule looks perfect. Orders are slotted. Commitments are made. And then reality shows up. A machine goes down. A key operator calls out. Setup times balloon. One late job cascades into five. Suddenly the plan (built meticulously inside your ERP) falls apart. Not because your team failed, but because the plan was never grounded in reality to begin with. The Hidden Lie Inside Most ERP Schedules

NetSuite’s Model Context Protocol (MCP), built in partnership with Anthropic, helps users leverage AI

Uncover the challenges of data quality affecting DIO accuracy, from ghost inventory to inconsistent formats. Find out how to tackle these issues effectively with a NetSuite ERP.

In the world of private equity, creating operational value has become increasingly critical as the market evolves. With exit timelines extending and competition for deals intensifying, PE firms are looking beyond financial engineering to drive returns. One emerging strategy that's gaining traction is the consolidation of NetSuite instances across portfolio companies. The Hidden Challenge of System Fragmentation As PE portfolios grow through acquisition, a common pattern emerges: multiple portfolio companies operating on separate NetSuite instances. While each system may work effectively in isolation, the fragmentation creates significant operational inefficiencies at the portfolio level: Redundant Licensing Costs: Each separate instance requires its own licensing structure , creating unnecessary expenses that directly impact EBITDA. Manual Consolidation Effort: Finance teams spend countless hours extracting, transforming, and manually consolidating data from disparate systems. Inconsistent Processes: Basic business functions are handled differently across portfolio companies, limiting standardization efforts. Limited Portfolio-Wide Visibility: Gaining insight across the entire portfolio requires extensive manual effort, delaying strategic decision-making. Integration Challenges: Onboarding new acquisitions becomes increasingly complex when each company maintains its own environment.